Welcome to

On Feet Nation

Members

-

freeamfva Online

-

Christopher Online

-

Alice Online

Blog Posts

lxputqpn

Posted by Frances on September 12, 2024 at 11:23pm 0 Comments 0 Likes

arsuyxuu

Posted by Steve on September 12, 2024 at 11:18pm 0 Comments 0 Likes

Ensuring Safe Transactions: A Guide to Buying WoW Gold

Posted by freeamfva on September 12, 2024 at 11:16pm 0 Comments 0 Likes

Introduction

World of Warcraft (WoW) is a game that has captivated millions of players worldwide. One of the key aspects of the game is gold, the primary currency used for various in-game transactions. While earning gold through gameplay is the traditional method, many players opt to buy gold to save time and enhance their gaming experience. However, buying WoW gold can be risky if not done correctly. This guide will explore… Continue

Top Content

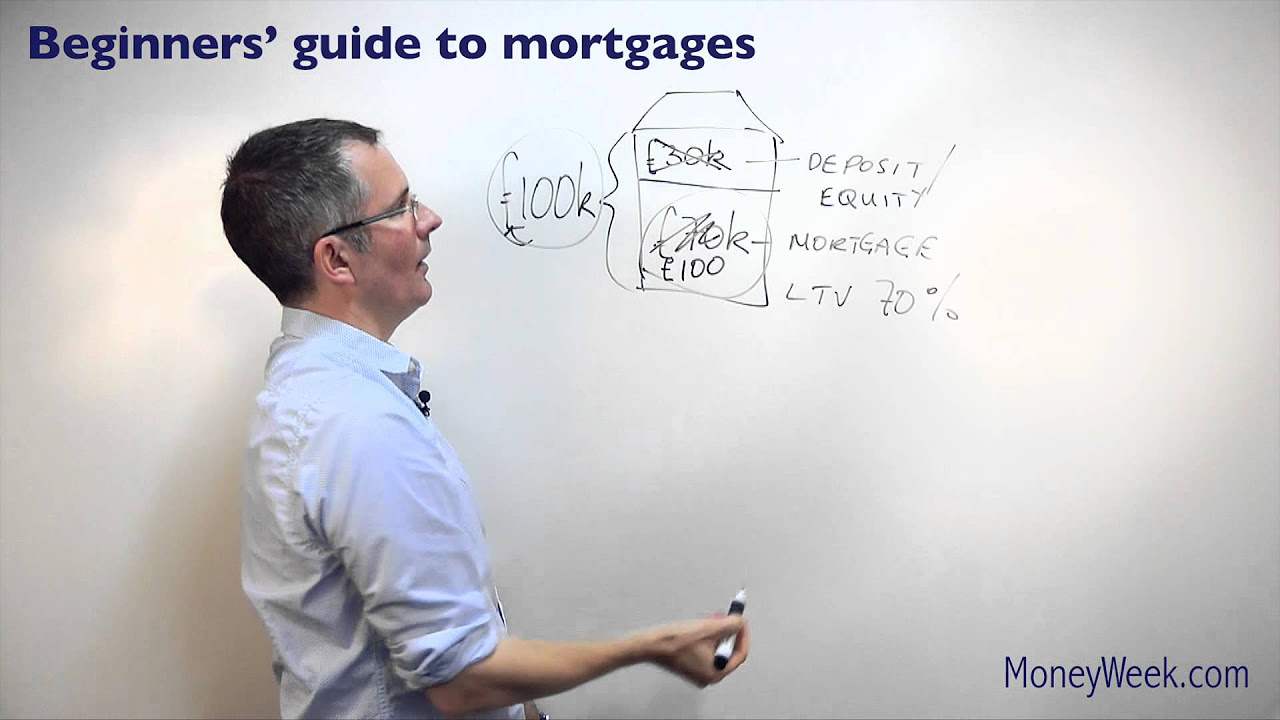

5 Killer Quora Answers on home loans

Preparing to look for a mortgage can be stressful, specifically if you don't understand where to start. You can get a excellent start simply from reading these 5 great mortgage tips for very first time house buyers.

1. Pay down your financial obligation.

Specifically, your credit card financial obligation. Why? Credit card debt is costly. The typical rate of interest for credit cards currently is 13.8%-- that's double the 5.33% average for a 30-year fixed rate mortgage. Charge card debt also aspects into just how much you can obtain. Lenders will not enable your overall monthly debt (which includes vehicle payments, student loans, property owner's insurance coverage, and property taxes in addition to a mortgage and credit cards) exceed more than 40% of your gross income.

2. Know your credit history.

Not ideal? Don't fret! In fact, purchasers can lastly capture a break. A few of the big gamers in the financing market have actually finally loosened their requirements, decreasing the minimum FICO score from 620 to 580 to qualify for a loan. Fannie Mae also uses an expanded approval program for those with a little blemished credit. You ought to always be mindful of precisely what is on your credit report before you start shopping for a mortgage. That way you can clear up any discrepancies or errors prior to lending institutions start making their queries.

3. Determine what you can manage.

Sadly, mustering up a down payment and after that writing a check on a monthly basis is just the beginning. You ought to also think about closing costs, which can be as much as 3% to 5% of your home's overall value, along with real estate tax and insurance. Funds for emergency situation house repair work are something else you should consider including. A general rule of thumb is that your mortgage, insurance, and taxes shouldn't surpass more than 28% of your gross income each year, which means that budgeting is crucial.

4. Don't settle immediately.

Shopping around does take time and energy, but it can save you thousands in the long run.

Rate of interest and charges differ greatly, so declining the very first loan provided can in fact be useful, although it may appear like shooting yourself in the foot. Compare loans from both lenders and brokers . Brokers set up loans with loan providers. They act as a go-between, so if you don't wish to deal directly with a lending institution, you might be interested in dealing with a broker.

5. Know your options.

Home loans can have various features. Some have adjustable rates, others have actually fixed rates. There are home mortgages where you pay Darwin Mortgage Northern Beaches only the interest for a while and after that pay for the principal, mortgages that charge a penalty for paying the loan off early, and home loans that have a balloon payment, or large amount, due when the loan ends. Being well informed about all your options will guarantee you discover the alternative that's right for you.

The typical interest rate for credit cards currently is 13.8%-- that's double the 5.33% average for a 30-year set rate mortgage. Lenders will not permit your overall month-to-month debt (which consists of automobile payments, trainee loans, property owner's insurance, and home taxes in addition to a mortgage and credit cards) go beyond more than 40% of your gross income.

You should always be conscious of precisely what is on your credit report before you begin going shopping for a mortgage. A general rule of thumb is that your mortgage, insurance coverage, and taxes should not surpass more than 28% of your gross income every year, which suggests that budgeting is key.

There are mortgages where you pay only the interest for a while and then pay down the principal, home mortgages that charge a charge for paying the loan off early, and home mortgages that have a balloon payment, or big amount, due when the loan ends.

Views: 2

Comment

© 2024 Created by PH the vintage.

Powered by

![]()

You need to be a member of On Feet Nation to add comments!

Join On Feet Nation